Leaking Money Series: Part Two – Shopping: Seven Shopping Behaviors That Are Draining Your Money

In this four-part series, we explore hidden ways people leak money and cover specific steps to “plug” the holes.

It's easy to lose track of spending when small habits add up. These seven shopping behaviors might seem harmless, but they're quietly draining your money—and could be holding you back from a stronger retirement:

- Online

- Social

- Boredom

- Retail Therapy

- Occasion

- Impulse

- Envy

- Status

Money has a funny way of disappearing. You work hard for it, save diligently, and plan for the future—but somehow, there never seems to be enough left at the end of the month. This phenomenon is known as "leaking money," the gradual and often unnoticed loss of funds through unnecessary expenses, inefficient financial habits, and lack of awareness. If left unchecked, it can have long-term consequences, especially for retirement savings. Unlike major financial mistakes, money leaks are typically small, recurring costs that add up significantly over time. Because they’re spread out and relatively minor individually, they rarely trigger alarm bells. However, their cumulative effect can be devastating to your overall financial health.

Hidden Ways Money Leaks while shopping (and actions to take)

There are many reasons we shop: needs, as an event, socializing, boredom, therapy, impulsive, envy, status. And many of these cause money leak. Not the kind you plan for, like groceries or back-to-school supplies—but the kinds that sneak up and chips away at goals. Here are some common shopping habits that might be costing you more than you think:

Online Ordering

It’s so easy. Think about something and it pops on a digital feed. Two clicks and the item is purchased before one even thinks if the item is actually needed. And even crazier – many times it arrives the same day. Too. Easy. Before online ordering, shopping meant physically going to the store, searching, maybe finding it, deciding, then a purchase. The physicality of shopping lessoned purchasing. One had to be committed. Now we can shop in our PJ’s.

Rule of Thumb: Wait 24 hours before completing any non-essential online purchase. This delay helps reduce impulse buys and gives you time to decide if you truly need or want the item.

Action: Log on to your shopping apps and review its history. How many of those items were actually needed? How many were actually used? How many are no longer even owned? How much money could have been diverted to other areas like debt reduction or future savings?

Make a list from the past three months of the items that went unused or were thrown away. What percent was that of the total? See if you can reduce online shopping by that much over the next month.

Play a game: Each month, try and reduce online spending by 10% (or more). How low can you get?

Additional Actions: Remove saved payment methods to make checkout less convenient. Unsubscribe from promotional emails that tempt you. Set a monthly online spending limit and track it like a budget category.

Example:

Judy reviewed her online accounts and found that about 15% of her purchases were unused. She averaged about $500 per month. Reducing her online ordering by 15% would save her ~$900/year

Social Shopping

It’s fun to browse the mall or scroll online with friends—but social shopping comes with subtle pressures. When everyone else is buying something new, it’s hard to resist joining in. That “sure, why not” purchase? It adds up, especially if it becomes a regular weekend activity.

Rule of Thumb: Bring cash and leave cards at home to limit spontaneous purchases.

Action: Suggest non-shopping activities when meeting up with friends (coffee, picnic, walk, game night); Set a monthly "fun money" budget and use it guilt-free—once it's gone, you're done.

Example

Judy met up with a set of friends once a month to get together. They typically walked through the mall (justifying as “exercise”). While shopping Judy always ended up finding something she “had to have” although didn’t even know it existed if not for their social get-togethers. When Judy went back and viewed her bank statement and credit cards, she realized she spent about $120 per month on social shopping ($1440/year). That was eye opening! She suggested to her friends to shop once a quarter and do other non-shopping get togethers in between, saving $960 per year.

Boredom Shopping

Scrolling through a favorite store’s app while waiting for dinner, wandering a store to kill time, or watching the shopping channel might seem harmless. But boredom can lead to mindless spending—grabbing things you don’t need just for a quick distraction. And those “little treats” quickly add up when they become a routine.

Rule of Thumb: Never shop when bored!

Action: Replace boredom shopping with a free hobby or activity—reading, walking, organizing, calling a friend; Block retail websites/apps during certain times with browser extensions; Create a “cooling off” list—if you want something, add it to the list and revisit in 72 hours.

Example

Stacie watched the shopping channel when she had “nothing else to do”. It was like having a personal shopper! She only indulged 3-4 times per month, thinking she was being reasonable. When challenged to add up her purchases, Stacie found she spent, on average, $55 per watch. That’s pretty good, she thought. Until she realized, none of those things she really used or wanted after the fact. Cutting her boredom shopping in half and replacing with other no-cost activities, would have saved Stacie $1160/year.

Retail Therapy

There’s a reason it’s called therapy—shopping can offer a temporary lift when we’re feeling low. When a person is sad or feeling bad the brain is looking for a hit of dopamine – the happy hormone. Some people find that dopamine by going shopping. And it works. But the happy hormone or emotional comfort doesn’t last, and purchases made in moments of stress, sadness, or frustration often come with a dose of regret later: both emotionally and financially. Financial wellness includes learning to soothe emotions in healthier, cost-free ways.

Rule of Thumb: no purchases when sad, mad, or tired.

Action: Build a feel-better toolkit that doesn’t cost money: journal, play music, go for a walk, take a bubble bath, call a friend, watch a funny movie, read a book, do something social; Recognize emotional triggers—stress, loneliness, fatigue—and find healthier responses.

Example

When Jonathan was down, a new electronic toy or tool did the trick. He justified it as a reward and a needed pick-me-up when he had a bad week or was stressed. When he looked at all the “therapy” electronics he purchased in the past year, (a new flat screen $478; the latest gaming console $499, and a new grill $499, and a new saw $560). When he looked back, he didn’t need any of them as he already had good ones. By reducing in half, Jonathan would have saved $1018 that year.

Shopping for Occasions

Shopping tied to birthdays, holidays, or big life moments can feel like part of the celebration. But when “special occasion” spending goes unchecked, it’s easy to go overboard. It often starts with one gift or outfit, and before long, the cart is overflowing with extras that weren’t on the list. Its easy to get swept away with the energy of the celebration, especially with all the marketing that gets you to believe you have to go big since its “only once a year”. But how many occasions are there throughout the year? They quickly add up.

Rule of thumb: if it takes more than one month to pay off occasion expenses – it’s too much. Reduce shopping to what can be paid for ahead of time.

Action: Set a budget before the occasion and stick to it; Plan purchases in advance to avoid last-minute splurging; Focus on meaningful experiences or gifts—not just expensive ones. Create a budgeted gift fund and “pay” into the fund monthly.

Example:

George and his wife had a plan of about $100 per kid (4) and grandchild (4) for December holiday. For others they didn’t have a set budget but figured between $20-$40 depending on what they found and the appropriateness of the relationship. In their mind, that meant a giving budget of around $1500. In January when reviewing their actual spend, George added up their purchases…. it was about $2500! And looking at birthdays, he estimated a spend of ~1500 (same basic budget as December), but when looking at what they actually spent… it was about $2500 as well! By sticking to their budget of $3000 for the year, George and his wife were able to save $2000 over the course of the year.

Impulse Buying

We’ve all done it—picked up something at the checkout or hit “buy now” during a flash sale. Impulse buys are rarely planned or budgeted, and because they happen so quickly, we don’t always recognize how often they occur. One or two here and there is fine; a pattern of them can eat through savings fast.

Rule of Thumb: For any item not on a budgeted list, add to a 72-hour waitlist. If still wanted/needed (and in the budget) then purchase.

Action: Unsubscribe from marketing emails and turn off app notifications; Shop with a list—and stick to it. Only impulse buy with cash from an “impulse fund”.

Example

Joann did the majority of the grocery shopping at a hypermarket superstore, the ones that combine groceries with a pharmacy, clothing, home décor & improvement, garden, electronics, etc. So, even though she shopped with a list, there was always something tempting merchandised at just the right spot as she passed, not to mention the extra’s while waiting at the checkout. Each week, when she grocery shopped, one or two items found their way in her cart, adding about $20 to her bill. That is $1,040 per year. If she could reduce those impulse buys by 50%, she would save $520/year.

Envy Shopping

Whether it’s a neighbor’s new patio set or an influencer’s latest fashion haul, it’s easy to feel like we’re missing out. Envy shopping happens when we buy things to match what others have, not because we truly want or need them. It’s a recipe for clutter, credit card debt, and dissatisfaction.

Rule of Thumb: Pause and pivot. Ask: Does this serve you? Or can you simply compliment the other person? This helps break the emotional impulse and reframe your mindset before you spend.

Action: Remind yourself of your financial goals and values—what are you working toward; Practice gratitude—daily reflection on what you already have can curb comparison; Unfollow or mute social accounts that trigger the “I need that too” feeling. Compliment instead of collecting.

Example:

Kevin’s work colleagues all drove nice new cars. Even those with lower positions drove nicer cars than he did. And his colleagues pressured him, they knew he could afford it. And it was tempting! It was about $300/month more then his current car. But then Kevin reminded himself that he focused on appreciating assets vs depreciating assets. He was focused on paying down his mortgage and to purchase some land. After focusing on his own goals, the temptation to buy a new car, just to compare favorably to others… no longer held any appeal.

Status Spending

We all want to feel successful—but when success is defined by brand names, luxury items, or the latest gadgets, it can come at a steep financial cost. Status spending often prioritizes appearances over actual financial health and can lead to ongoing pressure to “keep up” at the expense of long-term goals.

Rule of Thumb: Revisit personal goals when tempted to status spend. Does the purchase align with those goals? Then wait at least a week before status spending! Ideally one month!

Action: Ask yourself before purchasing: “Do I want this for me—or for how I think it makes me look?”; Focus on net worth, not net image—true wealth often doesn’t show on the outside; Set bigger, meaningful goals (debt-free living, early retirement, travel fund) and track your progress visibly to stay motivated.

Example:

Stephanie walked into an exclusive handbag shop in the airport. She had a great handbag, but wanted to “up” her game. She thought she would look more successful with a fancy bag. She justified that the purchase was an investment in her career, and bought the bag for $860.

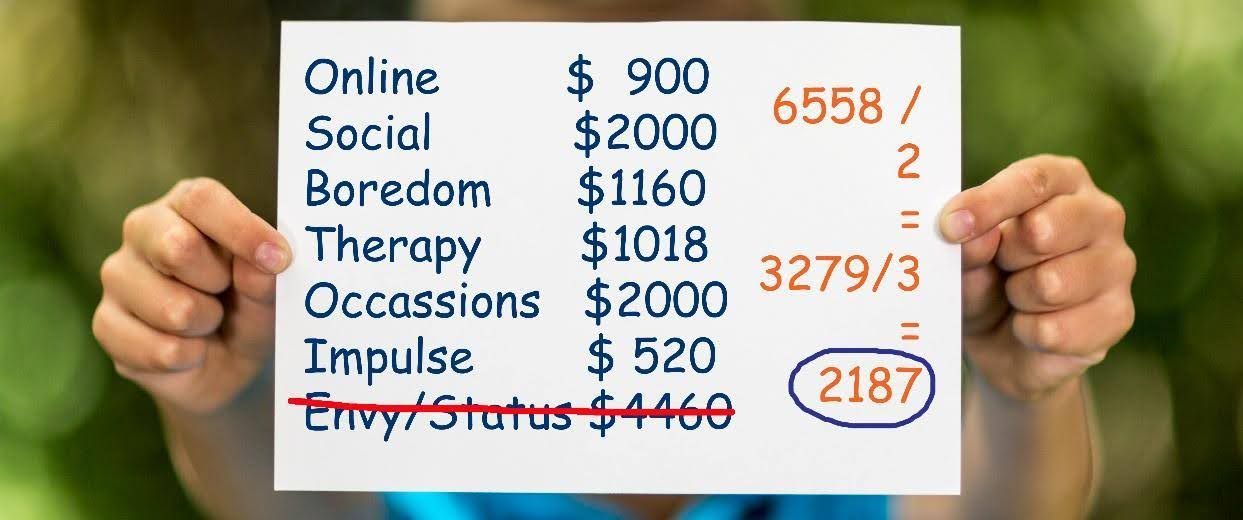

The Tally

With each of these shopping areas, the suggestion was to reduce. We all have times of increasing a shopping bill for one reason or the other. By reducing the amount spent in each area, vs removing altogether (although that is also an option!), there is the enjoyment of an unplanned find or social aspect, while also saving money. Using the suggested reductions, here is the end result:

Most of us only deal with some of these things, so let’s drop the tally down even more… cut it in half and remove the Envy/Status amounts. That is still $3279 over the course of the year that could have been saved… and invested!! If two-thirds were invested each year ($2187 - the other to debt pay-ff or emergency fund) at a 6% return over ten years, here is how much that leaking money would amount to:

$26,257

Know the Difference: Wants vs. Needs

Before you click "add to cart" or swipe your card, take a moment to ask:

Is this a want, or a need?

It sounds simple, but regularly making this distinction can drastically improve your spending habits—and your financial wellness.

- Needs are essentials: food, shelter, basic clothing, transportation, healthcare, and utilities.

- Wants are everything else: trendy shoes, the newest phone, dinners out, home décor, subscriptions, etc.

That doesn’t mean one can never buy wants—but recognizing them for what they are helps to stay in control of spending, instead of letting spending be in control.

Quick Action Tips:

- Pause and ask: “Do I need this to live or work, or do I just want it?”

- Delay want-based purchases by 72 hours (at least 24-48) to make sure it’s not just a fleeting urge.

- Budget “fun” money each month.

Understand marketing tactics

Brilliant minds strategize how to separate money from people. Understand what is being used against you so it is easy to recognize and make your own decision about what to purchase:

- Scarcity: limited quantity (buy now before its gone!); limited time offer/deal ends soon; countdown timers

- Using Emotion: many advertisers try to tap into insecurities, stir up discontent, show a solution to a problem or a “need” one didn’t even know they had (a don’t actually have).

- Fake Promises: another that taps into emotion – that by buying “this” a person will be successful, happy, etc.

- Product Positioning: typically, higher margin (and more expensive products) will be placed at eye-level. Make sure to look up and down for lower priced same products.

- Recommendations: many people get paid to recommend products. Be sure recommendations are real and from people who know you and what you are actually looking for.

Final Thoughts

Growing old is hard.

Most people imagine their future selves with the same energy, earning power, and health they have today—but aging brings real challenges. Work may not be as easy to come by. Health can decline. Energy fades.

That's why the sacrifices that feel tough right now—skipping impulse purchases, cutting back on non-essentials, rethinking wants vs. needs—are actually the easier path. Compared to the stress of trying to stretch every dollar in retirement, today's small adjustments are a gift to your future self.

Plug the leaks now, and you'll build a better life in retirement.